Introduction

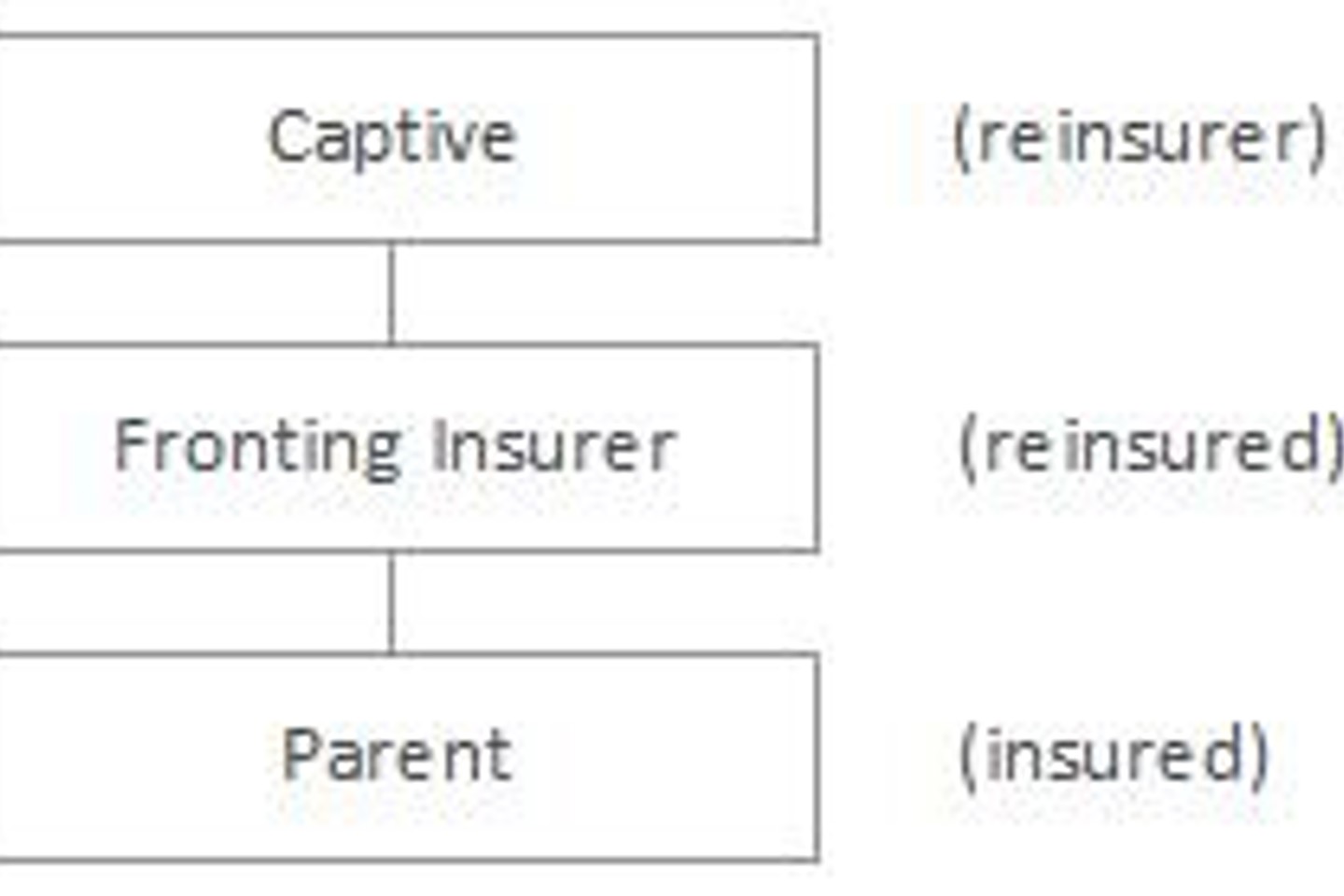

It is common for a Guernsey captive to reinsure a fronting insurer which in turn insures the captive's parent as follows:

Consequently, the issue of security is a common theme in Guernsey captive arrangements. Some of the security options available and some legal issues arising are considered below.

Letters of credit ("LOC")

Under an LOC, a bank issues a cash facility to the fronting insurer effectively guaranteeing payments due under the reinsurance. Although the LOC is issued in respect of the captive's obligations under the reinsurance, the bank need not concern itself with whether any payment requested by the reinsured is covered by the reinsurance. Provided the preconditions to payment on the fact of the LOC have been satisfied, payment will be made on demand.

Accordingly, even if the captive disputes that a claim is covered by the reinsurance it is unlikely to be able to prevent a reinsured from drawing down on a letter of credit in support, unless there is fraud.

However, although the LOC may not impose any preconditions as to payment, the reinsurance treaty might. Where it does, a breach of those terms may entitle the reinsured to an injunction preventing any drawdown – a good reason to include clearly LOC terms in the reinsurance treaty.

Although letters of credit provide first class security, they come at a price:

- bank fees will be payable;

- they tie up the captive's collateral and may therefore restrict investment income opportunities;

- over years, "stacking" can become a problem – where a policy is renewed and a new LOC is required for the renewal year while the LOC in respect of the previous year(s) must remain in place;

- fronting insurers are not always well motivated to reduce LOCs once in place, even for mature claim years; and

- bank credit ratings are not what they once were, and counterparty risk may be an issue for some insurers.

There are, not surprisingly, a number of cheaper, more flexible but generally less secure alternatives.

Security arrangements

A captive can grant security over its assets to the fronting insurer to back up its obligations under the reinsurance treaty. Helpfully, under section 2(6) of Schedule 2 to the Guernsey Insurance Law, an asset the subject of such security is still regarded as an approved asset for regulatory purposes. Where the assets are situated in Guernsey, security can be granted through a Guernsey security interest agreement.

In addition, there is at least one institution in Guernsey which currently offers a slightly more advanced form of security, a security trustee agreement, whereby a custodian is appointed over the relevant assets of the captive and security is granted in favour of a security trustee.

These arrangements provide a good form of security while charging lower fees than LOCs and more investment flexibility, however, lack of familiarity with these arrangements means some time may need to be spent educating the fronting insurer as to these structures. Undoubtedly, as these forms of security become more common, this issue will fade.

Cut through clauses

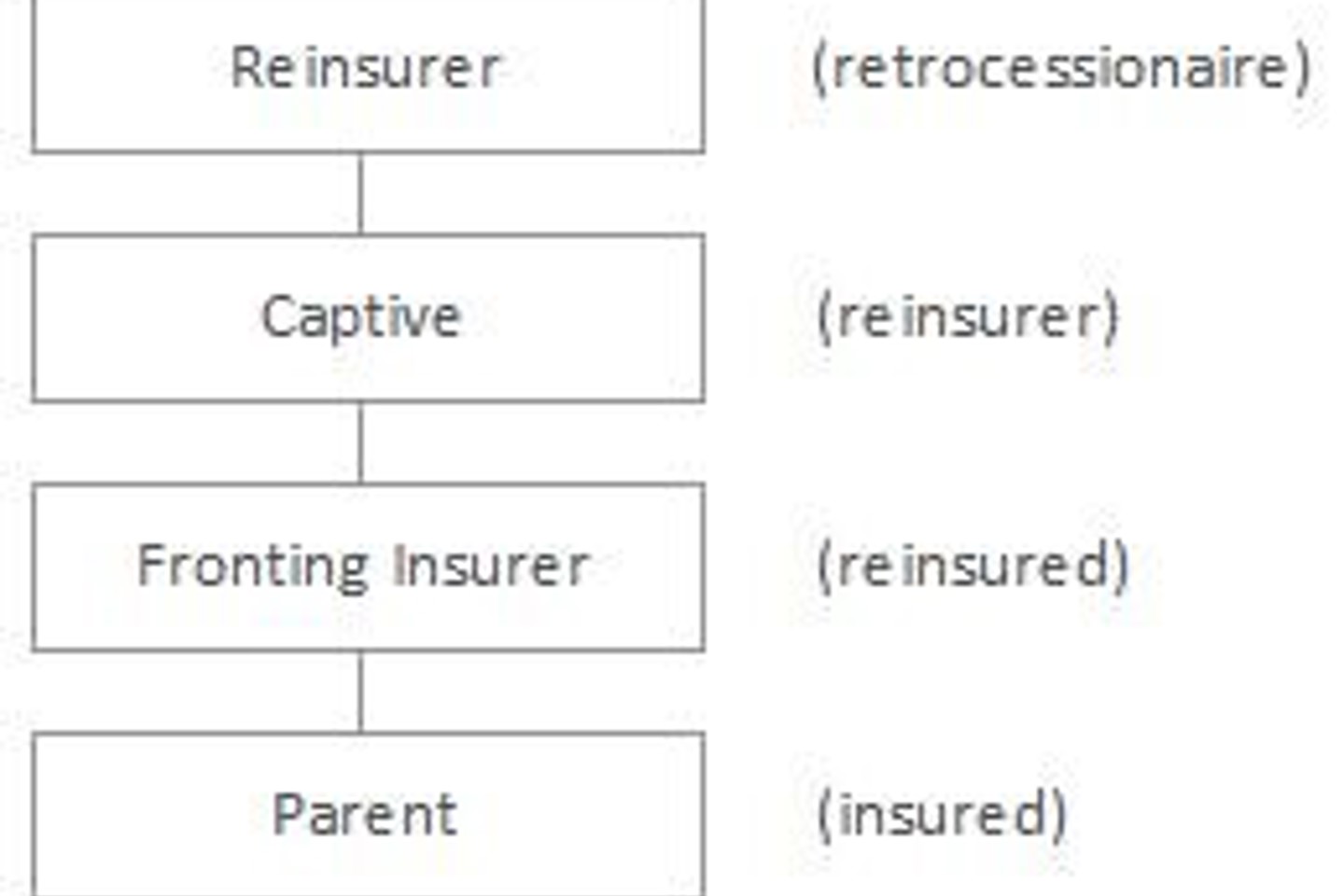

It is common for Guernsey captives to obtain retrocession to protect their own books of business as follows:

In this situation, the fronting insurer may include a cut through clause in the retrocession treaty, entitling the fronting insurer to claim directly from the captive's retrocessionaire in the event of an insolvency.

As a result of the privity of contract principle, care needs to be taken here. This principle means that a fronting insurer who is not a party to the retrocession cannot benefit from a cut through clause contained in it.

The enactment of the Contracts (Rights of Third Parties) Act 1999 amended the privity of contract principle in the UK. Under that law, the benefit under a contract could be conferred upon a person who was not a party to it. Accordingly, cut through clauses in reinsurance contracts governed by English law could benefit underlying insureds.

There is no equivalent of the Contracts (Rights of Third Parties) Act 1999 in Guernsey. Accordingly, the privity of contract principle continues to apply where parties wish to create such a cut through right in respect of a Guernsey law insurance or reinsurance agreement, they must take care to ensure that all relevant parties agree to the cut through.

Assign rights under reinsurance policies

Provided the retrocession does not prohibit assignment, the captive can assign its rights under it to the fronting insurer by way of security.

However, it should be noted that the fronting insurer can have no better rights under the retrocession than the captive and so if there were any grounds for the retrocessionaire denying cover to the captive (e.g. for non-disclosure) the retrocessionaire could equally deny cover to the fronting insurer.

In addition, if at the time the assignment was made, the captive was in financial difficulties, the assignment is at risk of being set aside as a preference to a creditor.

Premium trust arrangements

Under these arrangements premium payable to the captive by the fronting insurer is held in a separate account on trust for the benefit of the fronting insurer. Thus the funds are protected from other creditors on an insolvency of the captive. It is also possible for the captive to declare a similar trust over any recoveries it may make under retrocession treaties.

These arrangements are similar in effect to the cells of a PCC, where assets of each cell are protected from the insolvency of other cells. A trust is therefore more suitable for a single company captive writing multiple lines of business, or alternatively it is possible to convert a single company captive into a PCC and write different lines in different cells. Risks can also be segregated into cells by their nature (i.e. liability/CAT risk) or, for example by geographical region. This also enables profits to be split according to risk management performance in large global groups with varied business lines and operations. It is also possible to combine trust arrangements with PCC cells and/or letters of credit in combination.

The flexible approach of the Guernsey regulator means that assets held under trust in this way are still generally capable of being recognised as approved assets for regulatory purposes.

However, if these arrangements are entered into at a time when the captive is in financial difficulty they are at risk of being set aside as a preference.

Conclusion

There are a number of arrangements other than letters of credit which provide significant protection to a fronting insurer.

The recent growth in offshore jurisdictions which offer captives the ability to write insurance direct into the European Union without the need for a fronting insurer accentuates the need for Guernsey captives to continue to innovate in providing adequate security arrangements at reasonable cost.

Location: Guernsey

Related Service: Corporate & Commercial